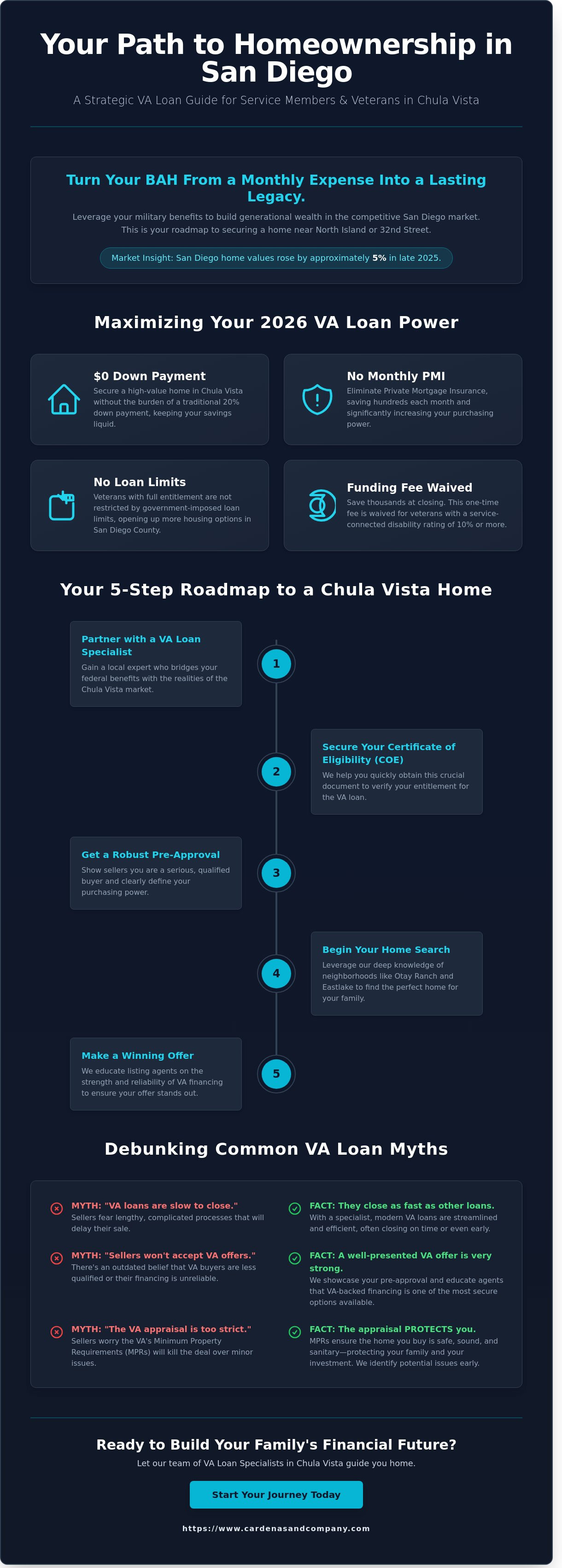

What if your monthly housing allowance was the catalyst for your family's long-term financial legacy rather than a recurring expense? For many service members stationed at North Island or 32nd Street, the transition to homeownership feels hindered by San Diego County's high cost of living and persistent myths about the VA appraisal process. Partnering with an expert VA loan specialist Chula Vista transforms these obstacles into a clear pathway toward stability. We understand that your move is not just a change of address; it's a strategic step for your future.

You already know that the local market demands precision and speed. We promise to show you how to leverage your $0 down benefits effectively while addressing the 2026 BAH adjustments with confidence. This guide provides a detailed roadmap for securing a home near base, debunking seller misconceptions, and building lasting wealth through real estate. We'll break down the latest affordability metrics and offer proven strategies to ensure your offer stands out in a market where San Diego home values rose by approximately 5% in late 2025.

Key Takeaways

- Understand how a dedicated VA loan specialist Chula Vista acts as a vital bridge between your federal entitlements and the unique nuances of the local real estate market.

- Learn to leverage 2026 benefits, including $0 down payments and the elimination of monthly PMI, to significantly increase your family’s purchasing power.

- Discover sophisticated strategies to overcome seller objections and position your VA offer as a secure, competitive choice in a crowded market.

- Master the essential pathway to homeownership by securing your Certificate of Eligibility and a robust pre-approval before you begin your search.

- Frame your property purchase as a strategic asset to ensure your military service translates into a lasting legacy of long-term financial security.

What Does a VA Loan Specialist in Chula Vista Actually Do?

A VA loan specialist Chula Vista serves as the vital link between your hard-earned federal benefits and the complex reality of the Southern California housing market. While many lenders can process a standard application, our role at Cardenas & Company involves a much deeper level of advocacy. We don't just see numbers; we see the beginning of your family's next chapter. We act as a bridge, translating the technicalities of the VA loan program into a competitive advantage during the home-buying process.

The difference between a generic loan officer and a local specialist is often measured in the success of your offer. A call center officer in another state won't understand why a home in Otay Ranch commands a premium or how to handle a specific VA appraisal issue unique to San Diego's older housing stock. We provide a structured and deliberate approach, ensuring every detail of your eligibility is verified long before you step foot in a showing. Our team proactively reviews properties for VA Minimum Property Requirements (MPRs). These are safety and habitability standards that every home must meet. By identifying potential issues like wood-destroying organisms or outdated electrical systems early, we prevent the anxiety of a failed appraisal late in the escrow period.

We believe in a collaborative approach. At Cardenas & Company, we view legal and financial success as a shared journey. We work alongside you to secure your legacy, providing the technical expertise required for compliance while maintaining the empathy needed to support you through a significant life transition.

Beyond the Pre-Approval Letter

A VA loan specialist Chula Vista acts as a strategic advocate who bridges the gap between technical military benefits and the competitive nuances of the local real estate market. We don't stop at issuing a letter. We communicate directly with listing agents to educate them on the reliability of modern VA financing. Many sellers still hold outdated beliefs that VA loans are slow or difficult. We dispel these myths by presenting a clear, data-backed case for your financial strength, ensuring your offer is viewed with the respect it deserves.

Local Expertise in San Diego and Chula Vista

Our team lives and works in the South Bay, offering deep knowledge of neighborhoods like Otay Ranch and Eastlake. We understand that for a service member, a home is more than an investment; it's a base of operations. We calculate commute times to Naval Base San Diego or North Island with precision, helping you balance neighborhood amenities with daily logistics. For more detailed insights into the transition process, you can explore our Comprehensive Guide to Military Relocation.

Maximizing Your 2026 VA Benefits in San Diego County

The 2026 real estate market in San Diego County presents unique opportunities for service members and veterans. We focus on leveraging the $0 down payment benefit, which remains the most powerful tool for building generational wealth in the South Bay. Because veterans with full entitlement no longer face government-imposed loan limits, you can secure a high-value home in Chula Vista without the burden of a traditional 20% down payment. You should first verify your specific status by reviewing the VA home loan eligibility requirements to ensure your Certificate of Eligibility (COE) is ready for the current fiscal year.

Eliminating Private Mortgage Insurance (PMI) significantly boosts your monthly purchasing power. Conventional buyers often pay hundreds of dollars each month for insurance that only protects the lender. As your VA loan specialist Chula Vista, we ensure you capitalize on this exemption, allowing those funds to go directly toward your principal or to offset current market interest rates. Most veterans will pay a one-time funding fee, which typically ranges from 1.25% to 3.3% depending on your down payment and prior usage. However, if you have a service-connected disability rating of 10% or higher, the VA waives this fee entirely, saving you thousands of dollars at the closing table.

Calculating Affordability in the South Bay

Your Basic Allowance for Housing (BAH) serves as the foundation of your mortgage application. San Diego BAH rates are adjusted annually to reflect local housing costs, ensuring your benefit keeps pace with the Chula Vista rental and sales markets. We help you calculate how much of your BAH can cover the mortgage while accounting for local variables. Chula Vista properties, particularly in newer developments like Otay Ranch or Millenia, often include Mello-Roos assessments and property taxes that average around 1.1% to 1.25% of the home's value. We analyze these numbers together to ensure your monthly payment remains sustainable for your family's future.

The VA Appraisal Process

The VA appraisal is often misunderstood as a hurdle, but it actually serves as a vital safeguard for your investment. The appraiser ensures the home meets Minimum Property Requirements (MPRs) regarding safety, sanitation, and structural integrity. If the appraisal comes in lower than the purchase price, we utilize the "Tidewater" initiative. This process allows your VA loan specialist Chula Vista to provide additional market data to the appraiser before the final value is set. We actively work to debunk the myth that these appraisals are deal killers. Instead, they provide a layer of protection that ensures you do not overpay for a substandard property. If you are ready to explore your options, our team can help you build a tailored homeownership strategy for the year ahead.

Winning the Offer: VA Loan Strategy in a Competitive Market

In the high-demand Chula Vista market, military buyers often face a hurdle that has nothing to do with their financial strength; it is the seller's perception. Many sellers harbor outdated fears that VA loans are bogged down by bureaucratic red tape or impossible repair demands. We bridge this gap by reframing the narrative. As your VA loan specialist Chula Vista, we don't just submit paperwork. We advocate for your right to use the benefits you've earned while protecting the seller's timeline.

A winning offer in 2026 requires more than a high price; it requires a "clean" contract. This means avoiding requests for minor cosmetic repairs that can trigger seller anxiety. We focus on the core strengths of the VA Home Loan Program, emphasizing that these loans are backed by the federal government and represent some of the most stable assets in the mortgage industry. Data from the Department of Veterans Affairs consistently shows that VA loans have lower foreclosure rates than conventional loans, a fact we use to reassure sellers of your reliability.

Cardenas & Company leverages deep-seated local relationships to get your offer to the top of the pile. When a listing agent sees our name, they know the file is meticulously prepared. We remove the "fear of the unknown" by providing a transparent roadmap from the initial offer to the final key exchange, ensuring peace of mind for all parties involved.

Closing the Education Gap with Sellers

Our team initiates proactive outreach to listing agents the moment an offer is sent. We explain that modern military buyers often possess credit profiles that rival or exceed those of conventional borrowers. By demystifying the appraisal process, we turn a perceived liability into a position of strength. If you are also considering Selling Your Home in Chula Vista, you understand the value of a buyer who is guaranteed to reach the closing table without financial surprises.

The Role of the Buyer Representation

You need an agent who understands the nuances of South Bay inventory. Whether you are looking at new developments near Otay Ranch or established South Bay San Diego Homes for Sale, the strategy changes. We ensure the home meets VA Minimum Property Requirements before you even sign the offer. This foresight prevents late-stage deal killers and builds immediate trust with the seller. Working with a dedicated VA loan specialist Chula Vista ensures you are not just searching for a house, but securing a legacy for your family.

The Step-by-Step Path to Chula Vista Homeownership

Buying a home in the South Bay requires more than just a desire to settle down; it demands a tactical approach. Your journey begins long before you step into an open house in Otay Ranch or Eastlake. Partnering with a dedicated VA loan specialist Chula Vista ensures that every technical requirement aligns with your long-term financial legacy. We view this process as a collaborative mission to secure your family's future through disciplined planning and expert advocacy.

Preparation and Documentation

Securing your Certificate of Eligibility (COE) stands as the indispensable first step that validates your service-earned benefit and sets the entire operation in motion. You'll need to gather your most recent Leave and Earnings Statements (LES), your DD-214, and 60 days of consecutive bank statements to provide a clear picture of your financial standing. A critical component of this phase is understanding the "residual income" requirement. Unlike traditional loans that focus solely on debt-to-income ratios, the VA mandates a specific amount of discretionary income remaining each month after all debts and housing costs are paid. This requirement serves as a protective buffer, ensuring you maintain a high quality of life while building equity in the 91910 or 91911 zip codes.

- Gather Documents: Organize your LES, DD-214, and two years of W-2s early to avoid processing delays.

- Verify Eligibility: Your VA loan specialist Chula Vista can often pull your COE instantly through the LGY portal.

- Calculate Residuals: Ensure your net income meets the regional threshold for the West Coast to guarantee loan approval.

Navigating Escrow and Closing

Once your offer is accepted, you enter escrow, which functions as a neutral third-party period typically lasting 30 to 45 days in the current California market. During this phase, the VA appraisal plays a dual role by determining fair market value and ensuring the property meets Minimum Property Requirements (MPRs). These standards focus on safety, sanitation, and structural integrity, protecting you from purchasing a property with immediate, costly defects. It's a layer of consumer protection that traditional buyers often lack.

Your final walk-through in Chula Vista is the last opportunity to verify that the property condition remains unchanged and that any requested repairs are complete. Regarding closing costs, it's vital to distinguish between what you can and cannot pay. VA regulations strictly prohibit Veterans from paying certain "non-allowable" costs, such as lender attorney fees or specific administrative charges. This regulatory framework keeps more capital in your pocket as you transition into your new home. We prioritize transparency during this stage to ensure you arrive at the signing table with absolute peace of mind.

If you're ready to begin your journey toward military homeownership, contact our team today to review your eligibility and start your pre-approval process.

Building a Legacy: Real Estate Wealth for Veterans

Owning a home in Chula Vista is more than a lifestyle choice. It is a strategic move for your financial future. In San Diego County, property values have historically shown resilient growth, often outperforming national averages over ten year cycles. We don't just see a house; we see a foundational asset that anchors your family's net worth. When you partner with a VA loan specialist Chula Vista, you gain an advocate who understands how to leverage your military benefits into long term wealth.

Christian Cardenas builds his practice on the principle of relationship driven real estate. This means we focus on your 2026 goals and beyond, rather than just the immediate transaction. We help you view your mortgage as a tool within a broader financial strategy. This approach considers how equity growth can eventually fund education, retirement, or future investment properties. We act as your proactive partners, ensuring your home purchase aligns with your vision for a secure legacy.

- Equity as an Engine: Your VA loan allows for zero down payment, but your monthly payments build an ownership stake in one of the most desirable real estate markets in the country.

- Strategic Advantage: We analyze local market trends to ensure you buy in areas with high potential for appreciation.

- Holistic Planning: Your home is the centerpiece of your financial portfolio, and we treat it with that level of technical precision.

Protecting Your Asset with a Living Trust

Securing a home is only the first step. Protecting that asset is equally vital. California's probate process can be notoriously long and expensive, often consuming a significant percentage of an estate's value in legal fees. We believe every military family should have a plan to bypass these hurdles. By establishing a trust, you ensure your home stays within your family without the interference of the court system. You can explore specialized resources for this at Trust San Diego to secure your family’s future and provide true peace of mind.

Next Steps for Military Families

The path to homeownership is a collaborative effort. We invite you to reach out for a zero pressure consultation where we can map out your specific timeline and goals. If you want to see the Chula Vista market in action, check out our YouTube Channel for detailed local tours and neighborhood insights. As your VA loan specialist Chula Vista, we are ready to guide you through this complex system with clarity and expert advocacy. Start your journey today and take the first step toward securing your military legacy.

Secure Your Legacy in San Diego County

Your journey toward homeownership represents more than a simple transaction; it's the foundation of your family's future security. Navigating the 2026 real estate landscape requires a strategic approach that prioritizes asset protection and long-term wealth. By mastering the technical nuances of your benefits and implementing a tailored offer strategy, you position yourself to win in the competitive South Bay market. Partnering with an experienced VA loan specialist Chula Vista ensures that every detail aligns with your personal goals. We focus on the individual story behind every military relocation, providing the meticulous advocacy you deserve. Our team brings specialized expertise to the South Bay market, acting as your proactive partner to transform complex systems into a clear pathway for your family's future. You've earned these benefits through your service, and now it's time to leverage them for lasting peace of mind.

Ready to use your hard-earned benefits? Contact Cardenas & Company Real Estate Group for a zero-pressure consultation

We look forward to helping you open this next chapter with confidence and clarity.

Frequently Asked Questions

Do I need a down payment for a VA loan in Chula Vista in 2026?

You don't need a down payment for a VA loan as long as the purchase price doesn't exceed the home's appraised value. In 2024, 90% of VA purchase loans were completed with zero money down, a benefit that remains a cornerstone of military homeownership in 2026. This program provides a direct pathway to owning property without the burden of decades of saving. We help you leverage this advantage to secure your family's future in the South Bay.

Can I use my VA loan to buy a condo in the South Bay?

You can use your VA benefits to purchase a condo if the Department of Veterans Affairs has already approved the specific complex. Chula Vista features 142 VA-approved condo developments as of late 2024. If a property isn't on the list, your VA loan specialist Chula Vista can submit a request for a project review. This process typically takes 30 to 45 days. We guide you through these technical requirements to ensure your investment meets all federal compliance standards.

How long does it take to close on a VA loan in San Diego?

The average closing time for a VA loan in San Diego County is 35 to 45 days. This timeline accounts for the mandatory VA appraisal and the rigorous underwriting process required to protect your interests. While some conventional loans might close in 30 days, the extra 5 to 15 days ensures your home meets safety and structural integrity standards. We maintain a steady rhythm throughout this period to provide you with peace of mind.

What are the VA loan limits for San Diego County in 2026?

There are no loan limits for veterans with full entitlement, meaning you can borrow as much as a lender approves without a down payment. For those with remaining entitlement, the 2024 limit for San Diego was $1,149,475. This figure is adjusted annually by the Federal Housing Finance Agency. By 2026, these limits will likely reflect the local market's growth. We analyze your specific entitlement status to create a tailored strategy for your purchase.

Can I have two VA loans at the same time if I move?

You can hold two VA loans simultaneously by using your remaining bonus entitlement for a second primary residence. This often occurs when a service member is reassigned and chooses to keep their first home as a rental property. You must meet specific income requirements and have enough entitlement left to cover the new purchase. We view this as a powerful tool for building your long-term legacy and financial security.

What if the VA appraisal comes in lower than the purchase price?

You can request a Reconsideration of Value or invoke the Tidewater Initiative if the appraisal is lower than the agreed price. In 2023, approximately 12% of VA appraisals required a Tidewater intervention. You have the right to provide three comparable sales to support the higher price. If the value doesn't increase, you can pay the difference in cash or negotiate with the seller. Your VA loan specialist Chula Vista acts as your advocate during these negotiations.

Is the VA loan only for first-time buyers?

The VA loan is a lifetime benefit that you can use multiple times regardless of your previous homeownership history. Statistics show that 45% of VA borrowers are repeat users who utilize the program to upgrade or downsize their homes. There's no limit on how many times you can access this benefit throughout your life. We focus on helping you navigate this system to secure a stable anchor for your family at every stage.

What are VA Minimum Property Requirements (MPRs)?

VA Minimum Property Requirements are safety and structural standards that a home must meet to qualify for government backing. These rules focus on three pillars: safety, sanitation, and structural integrity. A home must have functioning heating, a leak-free roof, and no lead-based paint. These requirements protect you from purchasing a property with hidden, costly defects. We ensure your prospective home aligns with these standards to safeguard your family's future.

Explore More from Cardenas and Company: