Why are so many high-net-worth families in San Diego still leaving their financial legacy vulnerable to a 37% top federal tax bracket and California’s aggressive state rates? Understanding the benefits of indexed universal life insurance is now a requirement for anyone looking to shield their wealth from the dual threats of market volatility and heavy taxation. In our local market, where real estate equity often represents a huge portion of net worth, staying liquid is just as important as staying profitable.

It's frustrating to watch your hard-earned savings sit idle or lose value during a market correction while your property equity remains locked away. We know that the lack of liquidity in traditional real estate can stall your next move. This guide shows you how a properly structured policy provides market-linked growth with a 0% floor, meaning you don't lose principal when the index drops. You'll see how families from Chula Vista to La Jolla use these strategies to create tax-free liquidity for future investments. We'll also break down current 2026 cap rates, such as the 10.75% limit seen on certain multi-index strategies, to help you decide if this fits your goals for long-term stability.

Key Takeaways

- Discover how to build tax-deferred wealth and access your cash value tax-free to shield your family's future from California's high income tax rates.

- Learn how the 0% floor provides a critical safety net, ensuring you never lose principal even when the S&P 500 or other market indices experience a downturn.

- Understand the benefits of indexed universal life insurance when using policy loans as a strategic liquidity engine for your next San Diego real estate purchase.

- See why integrating your policy with a Living Trust is essential for protecting your assets from creditors and lawsuits under California law.

- Identify the specific administrative costs and insurance fees you must monitor to ensure your long-term financial strategy remains transparent and efficient.

Table of Contents

What is Indexed Universal Life Insurance?

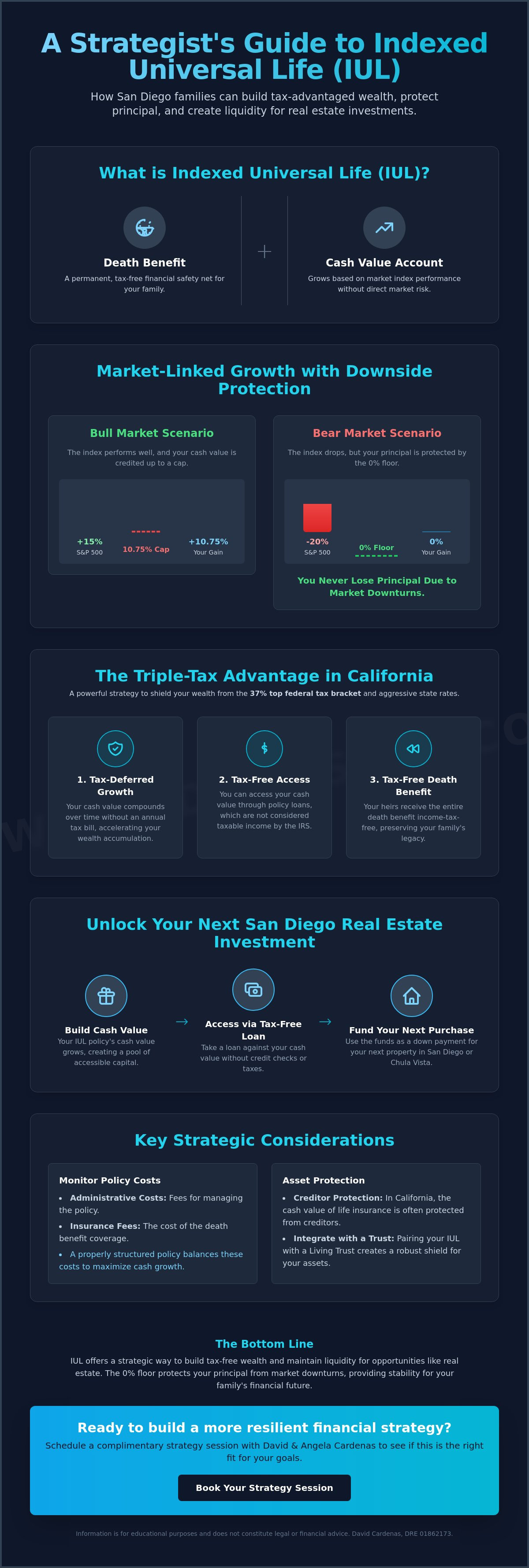

Understanding What is Indexed Universal Life (IUL) helps clarify why this is a favorite for those tired of market rollercoasters. Your policy includes a "floor," typically 0%, which acts as a safety net. If the market crashes 20%, your account simply stays flat for that period. You trade some of the unlimited upside of the market for the certainty that your balance won't drop due to index performance.

How Market-Linked Growth Works

The growth in your policy depends on participation rates and caps. A participation rate determines what percentage of the index's gain is credited to you. A cap is the maximum interest rate the company will credit during a specific period. For example, if the cap is 10% and the index grows 15%, you receive 10%. We track these movements using Basis Points, which is a technical term for one-hundredth of one percent. Even a shift of 50 Basis Points (0.50%) can impact your long-term accumulation, so we monitor these rates closely. This structure allows you to benefit from bull markets while avoiding the devastating losses of a bear market.

Universal Flexibility for San Diego Families

Life in San Diego moves fast, and your financial tools must keep up. IUL offers "universal" flexibility, meaning you can adjust your premiums and death benefit as your circumstances change. If you're a military family at Naval Base San Diego facing a PCS (Permanent Change of Station, or a mandatory relocation), you might need to lower your premiums temporarily during the move. This flexibility prevents the policy from becoming a burden during lean months.

You can also scale your death benefit down as your mortgage balance decreases or your children finish college. This level of control is why we act as your Trusted Advisor; we help you calibrate these settings to match your current cash flow. Whether you're watching the Chula Vista Bayfront development or planning your retirement in Eastlake, this flexibility ensures your policy remains a versatile asset. We focus on the practical, real-world impact of these choices on your family's long-term security.

Tax-Advantaged Wealth Accumulation in California

California's tax environment is notoriously challenging for families building a legacy. High-income earners in San Diego often see a massive portion of their growth eaten by state and federal taxes. In 2026, the federal income tax reaches 37% for income over $628,000 for single filers or $753,600 for joint filers. One of the primary benefits of indexed universal life insurance is the ability to shield your growth from these aggressive rates through a triple-tax advantage. Your cash value grows tax-deferred, you can access it tax-free through loans, and your heirs receive the death benefit without a tax bill.

This structure is why savvy investors in Southern California utilize IUL as a non-taxable wealth vehicle. Unlike a traditional brokerage account, you don't pay capital gains taxes every time your index strategy credits interest. FINRA's view on life insurance products highlights how these features manage both protection and accumulation. Keeping your money working without a yearly tax drag allows for much faster compounding over time.

The Power of IRS Section 7702

IRS Section 7702 is the federal code that defines what qualifies as a life insurance contract for tax purposes. It's the "secret sauce" that allows your policy to receive treatment that traditional 401ks or IRAs simply can't match. Most 401ks are a tax trap; you get a small break today but pay ordinary income taxes on every dollar you withdraw in retirement. IUL reverses this. By following Section 7702 guidelines, you can build a massive reserve and take "loans" against your own collateral that aren't considered taxable income. If you want to see how these tax strategies align with your San Diego property portfolio, we can help you review your financial roadmap.

Generational Wealth and Avoiding Probate

Transferring wealth in California is often a slow and expensive process. Probate is the legal process of validating a will and distributing assets. In the San Diego Superior Court, this can take nine months to two years, leaving your family in a state of financial limbo. During this time, they may struggle to pay property taxes or manage closing costs on inherited assets because their capital is tied up in the system.

An IUL death benefit bypasses Probate entirely. The funds go directly to your beneficiaries, usually within weeks of a claim. This immediate liquidity is vital for families in Chula Vista or La Jolla who need to maintain inventory levels in a family business or keep a real estate portfolio afloat. It ensures your hard-earned wealth stays within the family rather than being drained by court fees and legal delays.

Download

The Investor's Edge: IUL for Real Estate Liquidity

In San Diego, the ability to move quickly on a property often defines your success. One of the standout benefits of indexed universal life insurance is its function as a strategic liquidity engine. Traditional real estate equity is often "trapped" because it's locked in the walls of your home. By contrast, an IUL policy allows you to access cash through policy loans to fund down payments on residential properties without triggering a taxable event. This provides a bridge for investors who need to act fast when inventory levels shift in neighborhoods like Eastlake or Otay Ranch.

This strategy creates a powerful financial tool called arbitrage. When you take a loan from your policy, the insurance company uses your cash value as collateral. Your money stays in the index account, potentially earning interest based on current 2026 cap rates, such as the 10.75% seen in certain multi-index strategies. Meanwhile, you pay a lower interest rate to the carrier. You're essentially using the same dollar in two places at once. This is a massive advantage in the competitive South Bay market where "opportunity buys" require immediate capital to cover closing costs and securing the deal.

Becoming Your Own Bank

Borrowing against your policy is fundamentally different from a traditional bank loan. There is no credit check, and you have significant control over the repayment terms. This avoids the rigid Amortization schedules that can stifle your monthly cash flow. Amortization is the process of paying off a debt over time through regular payments. By bypassing traditional lenders, you increase the velocity of your money. You move capital from your policy into a cash-flowing asset and then back again. What is Indexed Universal Life Insurance? provides a technical deep dive into these loan mechanics for those who want to compare carrier options.

Strategic Growth in Chula Vista

We see investors leveraging this liquidity to participate in transformative local projects. The Chula Vista Bayfront project is a prime example of where quick capital can secure a foothold in a high-growth area. Imagine using your IUL cash value to secure a South Bay rental property while your principal remains protected from market volatility. You don't have to wait for a traditional mortgage to fund or for a house sale to close to have the cash you need. At Cardenas & Company, we host zero-pressure strategy sessions to show you how these insurance benefits integrate with your local property goals. It's about making your wealth work harder in the neighborhoods you know best.

Downside Protection and Risk Mitigation

Market volatility creates significant anxiety for families in San Diego. One of the core benefits of indexed universal life insurance is the guaranteed 0% floor. This protection means your account value is shielded from index losses. If the S&P 500 drops 15% in a single year, your principal remains exactly where it started. You don't have to wait for the market to "break even" before you see growth again, which is a major advantage for those nearing retirement.

The Floor and Cap Balance

Safe growth comes with a specific trade-off. Insurers set a "cap," which is the maximum interest rate you can earn in a single crediting period. In 2026, many carriers offer cap rates between 10% and 12% for S&P 500 strategies. For instance, the Nationwide YourLife® IUL currently features a 10.75% cap on its multi-index strategy as of March 15, 2026. This cap exists because the insurance company uses the budget from your premium to buy options that protect your downside. Conservative families often prefer this stability over the wild swings of direct stock market investing. It provides a way to participate in gains while avoiding the stress of a market crash.

Transparency in Policy Costs

We believe in radical transparency when discussing financial strategies. Every IUL policy carries internal costs, including administrative fees and mortality charges. Mortality charges are the actual cost of providing the death benefit based on your age and health. These are frequently referred to as the "Cost of Insurance." If these costs aren't managed through proper premium funding, the policy could face a lapse risk. A lapse is when the policy terminates because the cash value isn't enough to cover the monthly insurance costs.

Active oversight is the only way to ensure your policy stays healthy over decades. We use "zero fluff" reporting to help you read your IUL illustration and understand future cash value projections. You must know exactly how much of your premium goes toward growth versus internal fees. If you're ready to see a transparent breakdown of how these protections work for your specific situation, you can schedule a policy review with our group. This professional guidance helps you avoid common pitfalls and maximize the safety of your financial plan. We focus on the long-term health of your assets so you don't have to worry about shifting market conditions.

Integrating IUL into Your Asset Protection Strategy

One of the final benefits of indexed universal life insurance is the robust layer of asset protection it offers families in San Diego. While your real estate portfolio builds equity, it also carries liability. Lawsuits or creditor claims can threaten traditional savings accounts or brokerage funds. By contrast, California law often provides specific exemptions for life insurance cash value, making it a "safe bucket" for your wealth that is difficult for outside parties to reach. This legal shield ensures that your liquid reserves remain available for your family when they need them most.

A truly resilient legacy requires more than just high-performing assets; it requires a structure that prevents those assets from being drained by Probate or legal disputes. Probate is the court-supervised process of distributing your estate after you pass away. By combining your IUL policy with a Living Trust, you create a seamless transition of wealth. The death benefit flows into the trust tax-free and outside of the court system, providing immediate capital to handle property taxes or maintain your inventory levels of investment properties during a transition period.

Asset Protection in Southern California

Real estate owners in Southern California often have a high concentration of wealth in a single asset class. This lack of diversification creates a "liquidity trap" where you are rich on paper but cash-poor. We encourage our clients to link their insurance strategy to their Chula Vista home equity to balance this risk. Having a liquid, protected cash value account allows you to weather a market downturn without being forced to sell a property at a loss. It acts as a financial shock absorber for your entire portfolio.

Your Personalized Strategy Session

Moving from education to implementation is the most critical step in securing your legacy. David & Angela Cardenas specialize in reviewing your current portfolio to identify hidden risks and liquidity gaps that could derail your 2026 goals. Whether you are a military family at Naval Base San Diego or a seasoned South Bay investor, your strategy must be tailored to your specific timeline. We look at the "zero fluff" data to ensure your premium funding levels match your long-term objectives for growth and protection. Our team is here to help you navigate these complex systems as a collaborative partner, ensuring your transition into the next phase of your life is stable and certain.

Bottom Line: Indexed Universal Life insurance acts as a powerful shield for your wealth by combining market-linked growth with ironclad asset protection. Integrating this strategy with a comprehensive estate plan ensures your family's legacy remains secure against market shifts and legal challenges.

We invite you to join David & Angela Cardenas and the Cardenas & Company Real Estate Group for a private strategy session to review your portfolio. Visit cardenasandcompany.com or TrustSanDiego.com to begin securing your financial future today.

Information is for educational purposes and does not constitute legal or financial advice. David Cardenas, DRE 01862173.

Secure Your Legacy with Strategic Liquidity

The benefits of indexed universal life insurance provide a dynamic foundation for wealth that adapts to the high-stakes San Diego market. By layering market-linked growth with ironclad downside protection, you ensure your capital is never at the mercy of the next economic correction. This strategy transforms your insurance policy into a strategic liquidity engine, allowing you to seize local real estate opportunities as they arise. You gain the confidence to grow your assets while maintaining the flexibility needed for a South Bay lifestyle.

Building a secure future requires a partner who understands the unique pressures of Southern California taxation and property management. With over 25 years of local experience, including specialized service as military relocation specialists, we help you bridge the gap between complex financial theory and practical results. We focus on integrating these tools with your living trust to provide a seamless transition of wealth for the next generation. You deserve a plan that protects your family while empowering your investment goals.

Bottom Line: Indexed Universal Life insurance offers a unique combination of tax-advantaged growth and capital preservation for families in San Diego. It serves as a vital liquidity source for real estate investors while shielding principal from market volatility.

We invite you to a warm, zero-pressure strategy session with David & Angela Cardenas and the Cardenas & Company Real Estate Group to discuss your wealth goals. Visit cardenasandcompany.com or TrustSanDiego.com to secure your dedicated time today.

Information is for educational purposes and does not constitute legal or financial advice. David Cardenas, DRE 01862173.

Frequently Asked Questions

Can you lose money in an IUL policy?

You can lose money if the internal policy costs exceed the interest credited to your account. While the 0% floor protects your cash value from market losses, it does not stop the "Cost of Insurance" or administrative fees from being deducted. If you underfund the policy or if interest rates remain at the floor for several years, your principal could decrease. We emphasize radical transparency; you must understand that active management is required to prevent a policy from losing value over time.

How much does an Indexed Universal Life policy cost?

The cost of an IUL policy varies based on your age, health status, and the size of the death benefit you select. Premiums are flexible, meaning you can often adjust how much you contribute based on your current cash flow. Because we provide highly tailored strategies, we don't use "one size fits all" pricing. Instead, we focus on the minimum funding needed to keep the policy healthy while maximizing the benefits of indexed universal life insurance for your specific wealth goals.

Is IUL better than a 401k for San Diego residents?

IUL and 401ks serve different purposes and often work best when used together. A 401k provides an immediate tax deduction but creates a future tax liability at ordinary income rates, which can be a burden given California's high tax brackets. An IUL offers tax-free liquidity and downside protection that a 401k lacks. For many in San Diego, having a "tax-free bucket" of money provides a necessary hedge against future tax hikes and market volatility.

Can I use my IUL cash value to buy a house in Chula Vista?

You can absolutely use your cash value to fund a home purchase or cover closing costs. Closing costs are the various fees and expenses paid at the end of a real estate transaction. Many investors in Chula Vista use policy loans for down payments because it allows their original capital to continue growing through arbitrage. This strategy keeps your money moving and helps you compete when inventory levels are low in the South Bay.

What is the difference between IUL and Whole Life insurance?

The main difference lies in how interest is credited and the flexibility of the premiums. Whole Life offers a fixed interest rate and set dividends, while IUL links growth to market indices like the S&P 500 with a cap and a floor. IUL also allows you to adjust your premium payments and death benefit, whereas Whole Life typically has rigid, fixed requirements. IUL is often preferred by those who want more control and higher growth potential without sacrificing the safety of a floor.

How long does it take to build significant cash value in an IUL?

It typically takes 5 to 10 years of consistent funding to build significant, accessible cash value. This is not a short-term "get rich" tool; it is a long-term wealth strategy. The early years of the policy are focused on covering the initial costs of insurance and setting up the death benefit. Once you pass this initial phase, the compounding effect of market-linked growth begins to accelerate your accumulation.

Are IUL policy loans really tax-free?

Policy loans are tax-free because the IRS views them as a debt against your collateral rather than as earned income. This is one of the most powerful benefits of indexed universal life insurance for building wealth. As long as the policy remains active and is not a Modified Endowment Contract (a policy overfunded beyond IRS limits), you can access your cash without a tax bill. This liquidity is vital for managing property taxes or other sudden expenses without liquidating your real estate assets.

Do I need a medical exam to qualify for IUL in 2026?

Bottom Line: Indexed Universal Life insurance provides a versatile platform for growth and protection, but it requires professional guidance to manage internal costs. When structured correctly, it becomes a core asset for San Diego families looking to secure tax-free liquidity and long-term stability.

We invite you to schedule a zero-pressure strategy session with David & Angela Cardenas and the Cardenas & Company Real Estate Group to see how these tools fit your portfolio. Visit cardenasandcompany.com or TrustSanDiego.com to take the first step toward a more certain financial future.

Information is for educational purposes and does not constitute legal or financial advice. David Cardenas, DRE 01862173.

Disclaimer

The information provided on this blog is for educational and informational purposes only and does not constitute legal, financial, or investment advice. While we strive for accuracy, real estate markets and insurance regulations (including Living Trusts and IUL strategies) are subject to change. David Cardenas (DRE 01862173) is a licensed real estate salesperson; however, this content does not create an agency relationship. Please consult with a qualified attorney or tax professional regarding your specific situation.